Entrepreneurship is currently on the rise, largely driven by individuals who either are seeking to become their own boss or have decided to turn a passion into a full-fledged business. But how many of these small business owners have taken steps to protect the future of their businesses or have considered the legacy of their businesses after they die or retire? How many of them have included buy-sell agreements in their estate and business succession plans? When approached by business owners who wish to execute an estate plan, it is imperative that estate planning attorneys help these business owners take the necessary steps to protect the future of their businesses by ensuring that a well-drafted buy-sell agreement is a component of their plans.

What is a buy-sell agreement?

A buy-sell agreement is a legally binding agreement between the owners of a business and the business entity that details what will happen upon certain triggering events, typically the death, permanent disability, or retirement of one of the owners. Having a buy-sell agreement in place is important because it will prevent a withdrawing owner from freely transferring the owner’s ownership interest in the business to a third party without first offering the interest to the remaining owners or the entity.

Above is a screenshot of WealthCounsel’s Business Docx® drafting system, which includes a Buy-Sell Agreement option under the Mergers, Acquisitions, and Buyouts Suite.

What types of provisions should a buy-sell agreement include?

A well-drafted buy-sell agreement for a business should contain, at minimum, the following provisions:

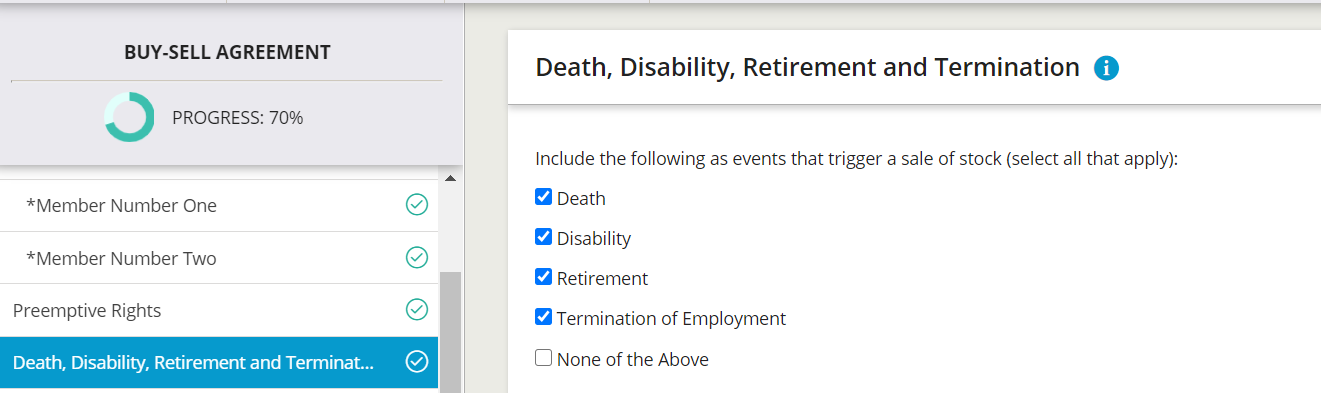

- the triggering events that will cause the business owner to sell or offer for sale the owner’s ownership interest in the business; can include not only an owner’s death, but also an owner’s permanent disability or retirement

Business Docx provides users the flexibility to select various types of triggering events.

- the purchase price of the owner’s interest and the formula for determining the purchase price (i.e., fair market value versus book value)

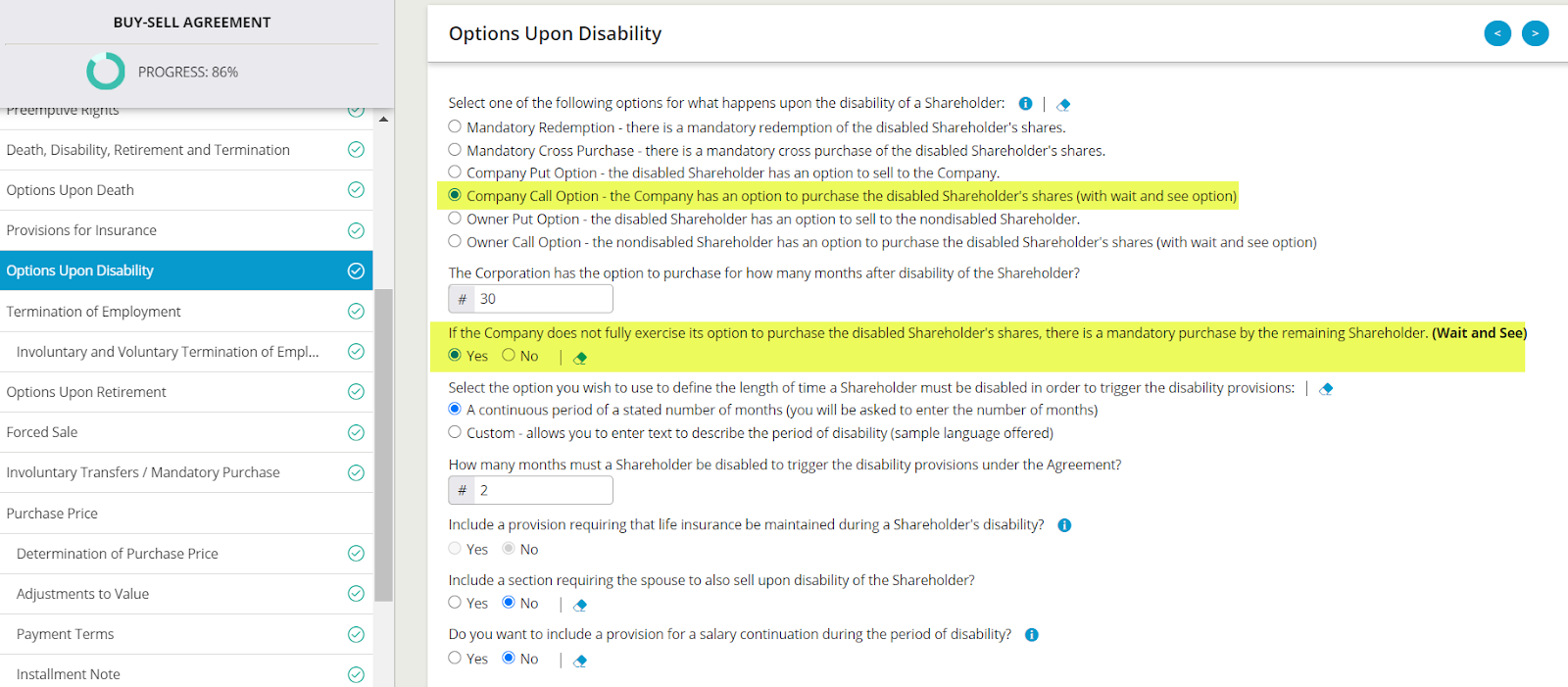

- the payment terms.

Above is an example of the payment terms offered within Business Docx.

What are the types of buy-sell agreements?

Each document in an individual’s estate plan is specifically crafted to meet the client’s goals, and a buy-sell agreement is no different. Selecting the right buy-sell agreement to draft for your client depends on the client’s goals, available funding, and taxes. Careful consideration and consultation with a client’s accountant is generally recommended before settling on the particular type of buy-sell agreement that fits the client’s goals. Generally, there are three types of buy-sell agreements:

Learn more about drafting buy-selling agreements by attending our webinar on November 11, 2020 at 1 PM EST.

- Entity purchase or stock redemption buy-sell agreement. This is an agreement between an owner and a closely held business entity. It requires the entity (the corporation, partnership, or limited liability company) to purchase, or have the right of first refusal to purchase, the interest of an owner upon the occurrence of a triggering event. This type of buy-sell agreement can be easily funded by obtaining a life insurance policy on the owner that the entity owns. The entity is also the beneficiary of the life insurance policy and pays the policy’s premiums. A major disadvantage of the entity purchase or stock redemption buy-sell agreement is that the surviving owners of the entity will not receive a step-up in basis on the value of their interests when the entity redeems the withdrawing owner’s interest.

- Cross-purchase buy-sell agreement. This is an agreement between the owners of the business in which they agree to purchase each other’s interest upon the occurrence of a triggering event. Again, life insurance policies are often used to fund the purchase of the withdrawing owner’s interest. A caveat, however, is that if there are several owners of the business, multiple policies are required to protect the various owners’ interests. If there are multiple business owners and multiple policies, this can be difficult to track and may make the administration of the agreement more difficult. However, an advantage of the cross-purchase buy-sell agreement, as compared to an entity purchase or stock redemption buy-sell agreement, is that the business owners in a cross-purchase agreement will receive a step-up in basis on the interest they purchase from the withdrawing shareholder.

- Wait-and-see or hybrid buy-sell agreement. This agreement is a combination of the other two buy-sell agreement types and is often used when there is not a life insurance policy in place to fund the transfer of the ownership interest in the business. While this type of agreement should still specify triggering events, the purchase price, and payment terms, it does not determine in advance whether the entity itself or one of the owners will be the purchaser. Typically, though, hybrid buy-sell agreements give the entity the right of first refusal to purchase the withdrawing owner’s interest.

No matter which type of buy-sell agreement is executed, the advantages of having an agreement in place strongly outweigh the disadvantages. Thus, ensure that you convey the following benefits of buy-sell agreements to your business owner clients:

- prevent withdrawing owners from selling their interests to a third party without the other owners’ consent

- minimize conflicts between owners because a plan is in place

- give business owners more security in preparation for retirement

- confer certain tax benefits for the business owners

- make banks and other lenders more comfortable extending credit because the future of the business is secure

- cover the expenses of finding a replacement owner

- cement the business’s core values and principles

- support the family of a deceased owner with the money from the transfer of the business interest after the owner’s death

We often meet with clients who have a clear and definitive vision of how they want their assets to pass to their loved ones. Unfortunately, business owner clients often have not similarly considered how they want their businesses to continue after they are gone. Buy-sell agreements offer multiple benefits for clients who have worked hard to establish their businesses and are concerned about the fate of their businesses in the event of death, disability, or retirement.